Variable Life Insurance

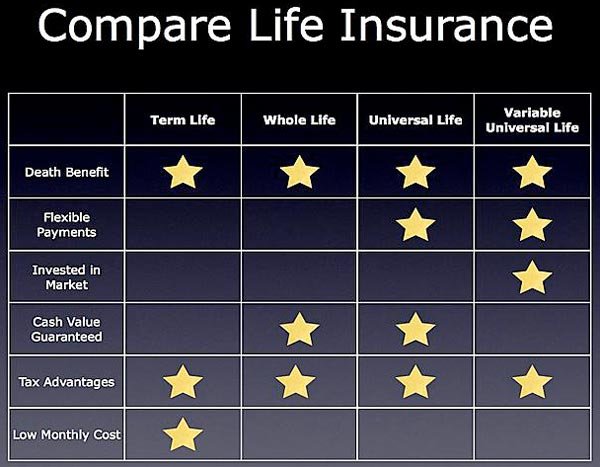

Permanent life insurance is a term for life insurance plans that, unlike term life insurance, doesn’t expire and by combining a death benefit with a savings portion, can build a cash value. The policy owner can borrow funds against this cash value, and in some instances, they can withdraw the cash value to help meet future goals such as paying a child’s college tuition.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

However, there is usually a waiting period after the purchase of your policy if you want to borrow against the savings portion of permanent life insurance. This is because a certain period of time has to pass in order for sufficient cash value to accumulate.

These life insurance policies also have favorable tax treatment. This means you don’t pay any taxes on any earnings in the policy as long as your policy stays active. If you stick to certain premium limits, you can take money out of the policy without being subjected to taxes. As long as you don’t exceed the number of premiums paid when you’re withdrawing funds, you won’t be taxed.

Variable Life Insurance Policy

Variable Life Insurance Policy

A variable life insurance policy is a type of permanent life insurance. It enables permanent protection to the beneficiary after the death of the policyholder. This type of insurance is often more expensive than term life insurance. It allows the insured person to transfer a portion of the premium dollars to a different account that consists of various instruments and investments inside the insurance company’s portfolio. These can be in the form of equity funds, money market funds, stocks, bonds, and bond funds.

However, just like with any other investment, there are risks. That’s why variable policies are regulated under the federal security laws as they are considered as securities contracts. As such, fund performance may lead to the decline of cash value or death benefit over time.

When it comes to tax benefits that were made available a to policy holders of variable life insurance, they have the ability to apply cash value on a tax-benefited basis. As long as they pay the premiums and the policy remains in force, the policy holder can access the cash value through a tax-free loan. However, if the cash value isn’t borrowed but instead withdrawn, the policyholder will face tax implications on any realized earnings. If a loan that’s taken out isn’t repaid in due time, the death benefit paid to the beneficiaries, which gets paid after the insured person passes away, will most likely decrease.

Variable Life Insurance Flexibility

A thing that makes variable life insurance different from permanent life insurance policies is the flexibility it provides to the policyholder in terms of premiums paid and cash value growth. Here, the premiums paid to traditional life insurance policies are not fixed. They can increase or decrease within certain limits over time, all based on the insurer’s needs. For example, if a person who has a variable life insurance policy decides that they want to reduce the monthly premium payment because they have an expense that they can’t cover without reducing the payments, they can do it.

The shortage in the premium payments can be covered by the cash value within the policy. And when the cash flow has returned to normal, the policy user can continue paying the initial fee of the payments.

Downsides of Variable Life Insurance

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Just like with any other good thing, variable life insurance has its downsides. Unlike fixed life insurance, variable life insurance may require the policyholders to, over time, add premiums to make sure the death benefit stays guaranteed to a certain age. If you pay more than the minimum cost of insurance for this type of insurance policy (which is usually around $100) you will probably insure that the guarantees remain intact.

Another thing to be aware of is that the investment risks within the cash value of this type of insurance falls completely on the policyholder and not on the insurance company. This is why there are now guarantees to how well the cash value will perform over time, so it is practically impossible to plan how the money will be used in the future after it’s paid back to the beneficiary.

And just like with any other life insurance policy, if someone wants to take out a variable insurance policy, they need to undergo a full medical exam.

More in Motivation

-

`

Amanda Bynes Pregnant at 13? Debunking the Rumors

Amanda Bynes Pregnant at 13? Debunking the RumorsIn recent years, the internet has been ablaze with rumors surrounding former child star Amanda Bynes, particularly regarding allegations of a...

July 1, 2024 -

`

Can Baking Soda Clean Your Lungs?

Can Baking Soda Clean Your Lungs?Years of inhaling cigarette smoke, pollution, and other toxins can leave you longing for a way to cleanse your lungs. The...

June 27, 2024 -

`

How to Build Muscle Mass After 60? 5 Proven Strategies

How to Build Muscle Mass After 60? 5 Proven StrategiesCurious about how to build muscle mass after 60? You are not alone. And the good news is that it is...

June 20, 2024 -

`

Prediabetic Foods That Can Lower Your Blood Sugar in 2024

Prediabetic Foods That Can Lower Your Blood Sugar in 2024Prediabetes is a health condition characterized by blood sugar levels that are higher than normal but not high enough to be...

June 13, 2024 -

`

Kelly Clarkson’s Weight Loss Journey | Here Are the Details

Kelly Clarkson’s Weight Loss Journey | Here Are the DetailsKelly Clarkson’s weight loss has been a hot topic among fans and media alike. The iconic American singer and host of...

June 3, 2024 -

`

Essential Vitamins for Gut Health – A Comprehensive Guide

Essential Vitamins for Gut Health – A Comprehensive GuideOur gut does more than just digest food – it plays a vital role in immunity, mood, and overall health. But...

May 30, 2024 -

`

Looking to Build A Stronger Sculpted Back? Try Cable Back Workouts

Looking to Build A Stronger Sculpted Back? Try Cable Back WorkoutsBack workouts using cables, or cable back workouts as they are commonly known, have become the gold standard for anyone aiming...

May 22, 2024 -

`

How Much Water Should I Drink on Creatine? Hydration Tips

How Much Water Should I Drink on Creatine? Hydration TipsCreatine, a popular supplement among athletes and fitness enthusiasts, has gained widespread recognition for its ability to enhance muscle strength, power,...

May 17, 2024 -

`

What Is Bruce Willis’s Net Worth? Get the Inside Scoop Here!

What Is Bruce Willis’s Net Worth? Get the Inside Scoop Here!Bruce Willis, the action hero who has saved the day countless times on screen, has built a legendary career. But how...

May 11, 2024

More From TelehealthDave

-

Fitness5 ‘Bad’ Fitness TikTok Trends You Shouldn’t Follow

Fitness5 ‘Bad’ Fitness TikTok Trends You Shouldn’t FollowTikTok has become a haven for creative fitness advice. But not all trends are worth your time or your health. From...

November 23, 2024 -

Nutrition & Weight LossDoes Drinking Water Affect Adrenal Hormones?

Nutrition & Weight LossDoes Drinking Water Affect Adrenal Hormones?Drinking water is often seen as a simple way to stay hydrated, but it has deeper effects on our body than...

November 14, 2024 -

MotivationWhy We Feel the Loss of Celebrities So Deeply?

MotivationWhy We Feel the Loss of Celebrities So Deeply?Celebrity grief might sound strange at first. After all, most of us have never met these famous figures in person, yet...

November 5, 2024 -

Health InsuranceAre High Deductible Insurance Plans as Ideal as They Appear to Be?

Health InsuranceAre High Deductible Insurance Plans as Ideal as They Appear to Be?High deductible insurance plans have been a hot topic for years, especially as healthcare costs continue to rise. For many Americans,...

October 31, 2024 -

FitnessHow Training Load Data Can Transform Your Exercise Routine

FitnessHow Training Load Data Can Transform Your Exercise RoutineTracking progress during workouts is challenging. Simple metrics like mileage or time don’t show the whole picture. Understanding the overall effort...

October 26, 2024

You must be logged in to post a comment Login